Another Bretton Woods?

Looking for logic in our trade policy

Martin Wolf has a piece in the Financial Times that tries to make sense of the Trump administration’s policies regarding trade and exchange rates. It’s a confusing article, but that’s not Wolf’s fault. It is difficult to find any sort of coherent policy. I keep thinking of that scene in Apocalypse Now:

Kurtz: Are my methods unsound?

Willard: I don't see any method at all, sir.

Here’s Wolf:

Donald Trump’s chaotic trade policy can only lead to economic chaos. So, might the Trump administration stumble upon something both more coherent and less damaging, yet still meet the president’s protectionist aims? Perhaps. Some members, including Scott Bessent, Treasury secretary, and Stephen Miran, chair of the Council of Economic Advisers, believe so.

If one is to understand this more sophisticated approach, one should read Miran’s “A User’s Guide to Restructuring the Global Trading System”, published in November 2024.

So I took a look at this user’s guide, and found the following:

It’s worth noting that value-added taxes are a form of tariffs because they exempt exported goods but tax imported goods, and central banks usually do not respond to them, because legislated price changes are typically thought not to be indicative of underlying supply-demand imbalances. (Indeed, the fact that other countries have VATs and we do not says something about initial conditions.)

Public Finance 101 says this is wrong. A VAT is a consumption tax. It excludes exports and includes imports because exports are not a part of domestic consumption and imports are. A VAT differs from a tariff in that the tax applies equally to both domestically manufactured goods consumed locally and imported goods consumed locally. Perhaps I’m missing something (and please help me out if I am), but Miran’s remark makes no sense to me.

And it’s all downhill from there. Miran expects foreigners to play a major role in paying off our national debt. Remember when conservatives were skeptical of free lunches? Yes, depending on elasticities foreign exporters might bear a portion of the tax, just as gasoline retailers might bear a portion of the gasoline tax. But it is reasonable to assume that motorists will largely avoid higher prices from a gas tax hike?

Returning to Wolf’s article, I found the following:

Underpinning Miran’s argument is a proposition made by the Belgian economist Robert Triffin in the early 1960s. Triffin argued that the growing demand for dollars as a reserve asset could only be supplied by persistent US current account deficits. This in turn meant that the dollar was persistently overvalued relative to the requirements of equilibrium in the balance of payments.

Over time, he argued, this weak trade performance would undermine confidence in the fixed dollar price of gold. So, indeed, it proved. In August 1971, in response to a run on the dollar, President Richard Nixon suspended gold convertibility.

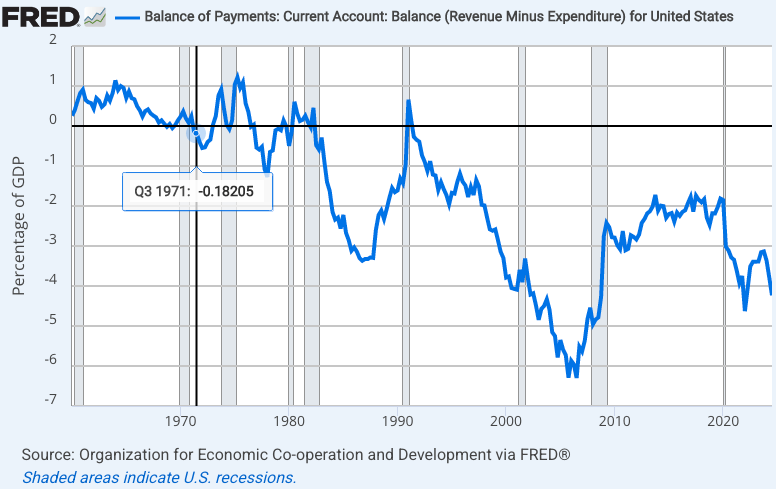

Unfortunately, this is factually incorrect. The Bretton Woods system did not lead to persistent US deficits, both the trade account and the current account registered surpluses under Bretton Woods, which ended only after Bretton Woods collapsed in 1971:

And then Wolf adds:

What is proposed now is recreating a global system of exchange rate management.

The justification for this, argues Miran, is that, as in the 1960s, the desire of most other countries to hold the dollar as a reserve currency is driving up its value and so opening a huge current account deficit.

Again, this never happened. The actual problem in the 1960s was an excessively expansionary monetary policy, which caused gold to be undervalued at the official $35/ounce peg, originally set in 1934. Not surprisingly, countries like France began to exchange dollars for gold, correctly anticipating that the peg would not hold. Trade was not the problem.

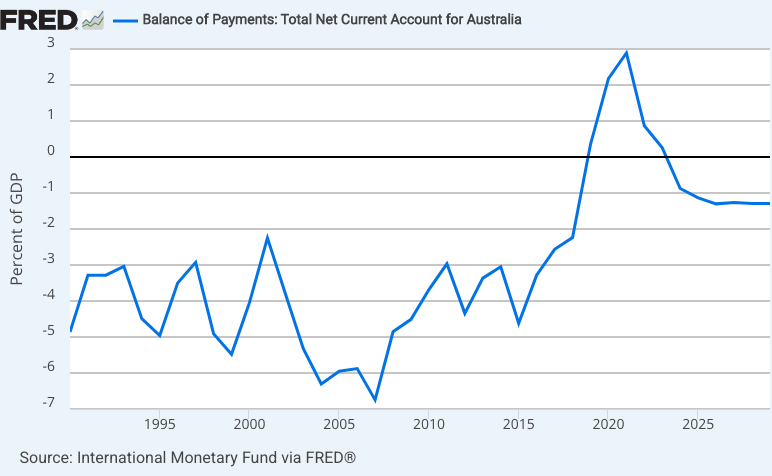

Our current account deficit is not caused by the dollar’s reserve status; it’s caused by a saving/investment imbalance. The Australia dollar is not a major reserve currency, and yet Australia has also run fairly persistent current account deficits:

I’m not sure why their deficit has recently gotten smaller—perhaps it is related to heavy immigration from high-saving Asia.

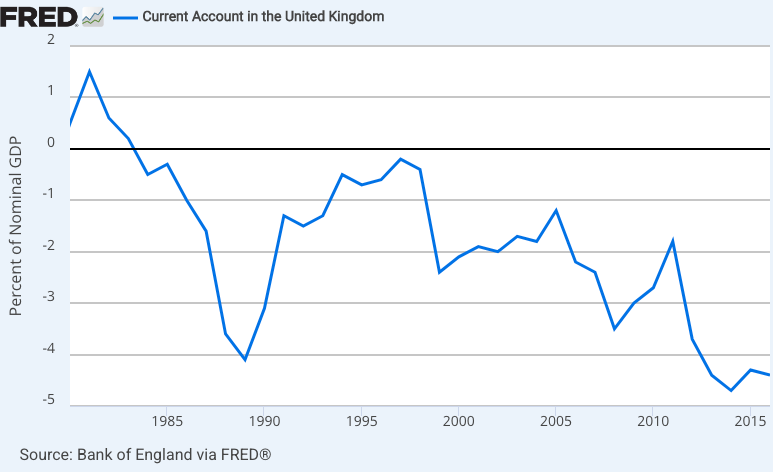

The British pound used to be a major reserve currency, but is no longer. And yet its current account is getting “worse”:

I use scare quotes for “worse”, as there’s nothing wrong with current account deficits.

Miran seems obsessed with the manufacturing sector:

MALIA: Make America Like Italy Again.

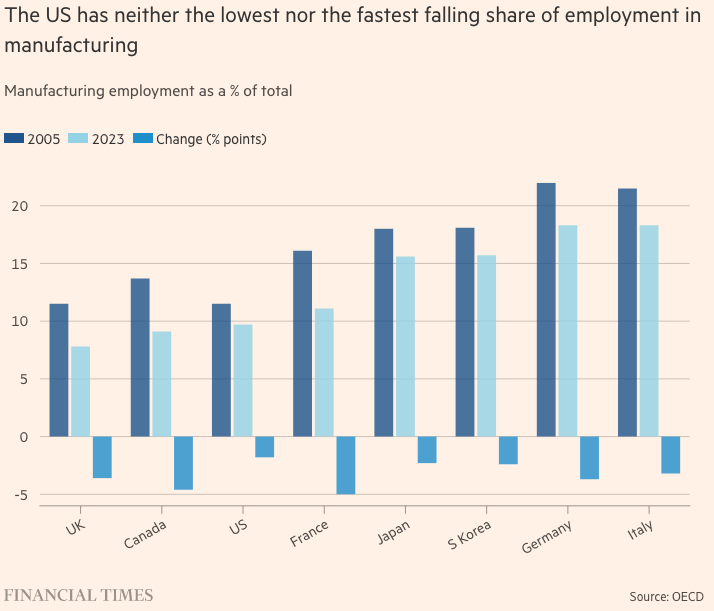

Seriously, Wolf points out that the US has actually had the smallest decline in manufacturing employment since 2005. This is a global trend.

Thus, the aim of a stronger manufacturing sector, to be delivered by a combination of tariffs and a weak dollar, needs global co-operation. My colleague, Gillian Tett, has described possible details of such a “Mar-a-Lago accord”.

It has two key aspects. The economic aspect is to release the constraints discussed above. The way to do so, suggests Miran, is to turn short-term borrowing into ultra-long-term borrowing, by “persuading” foreign holders to switch their holdings into perpetual dollar bonds. This would allow the US greater room to pursue its desired combination of loose fiscal and loose monetary policy. The political aspect is to point out that accepting such a deal would be the price of being viewed as a friend. Otherwise, a country would be viewed as a foe, or at best as floating in between. In a precise sense, this might be viewed as a “protection racket”.

Younger readers have no idea how demoralizing it is for an old guy like me to read something like this. Robert Mundell must be rolling over in his grave. The old Republican supply-siders used to argue for loose fiscal (tax cuts) combined with tight monetary policy. But loose fiscal and monetary policy? When has that ever worked? We’re going to run big budget deficits and the money-printing machine and prevent inflation by adjusting the term structure of our debt? I had thought “operation twist” was discredited in the 1960s. Have we learned nothing in the past 60 years? This is beyond even MMT.

The following is from the Gillian Tett article that Wolf linked to:

But what investors must grasp right now is that Trump’s recent actions are not “just” capricious; his team’s vision has a potent internal logic. The current chaos is as much a feature as a bug.

Or, to put it another way, when Bessent declared last year that he wanted “to be part of . . . Bretton Woods realignments” for the global finance and trade system, he was not joking. Far from it. The ongoing tariff shocks may presage a bigger drama. Watch out for that Plaza anniversary.

Oh good, more “drama” ahead.

"Do I really look like a guy with a plan. You know what I am. I'm a dog chasing cars. I wouldn't know what to do with one if I caught it. I just do things."

Joker, The Dark Knight

I would argue that the savings imbalance isn’t causal. It’s actually a result of America’s huge foreign equity investment profits, which are partially reinvested. Foreigners have to keep pushing capital into the U.S. just to keep the earning power of their international investments from falling behind ours.

For decades, net savings have flowed into the U.S. but we haven’t lost earning power over time. The market value of our foreign assets is much larger than the book value.