Economic insights

Where I get my ideas

People occasionally ask me where I get ideas for blog posts. So I thought I’d describe a few examples to illustrate how my vision of economics differs from that of many other economists.

What is economics? Some economists seem to visualize the field as a set of mathematical models. In my view, these models are overrated. Yes, it’s worth writing down a few simple mathematical models to clarify key economic concepts, but most of the more complex models are almost useless for understanding the macro economy. What good were DSGE models when the economy was falling apart in September 2008?

I view my field as a set of economic insights, ways of looking at the world. These include opportunity cost, comparative advantage, supply & demand, compensating differentials, transactions costs, arbitrage, efficient markets, rational expectations, national income accounting, etc., etc. These insights are tools that are useful in understanding the complex and messy world of reality.

Let’s start with a quote from some personal notes by George Warren, an economist who advised President Roosevelt back in 1934:

“The President (a) wanted more inflation and (b) assumed or had been led to believe that there was a long lag in the effect of depreciation. He did not understand–as many others did not then and do not now–the principle that commodity prices respond immediately to changes in the price of gold.”

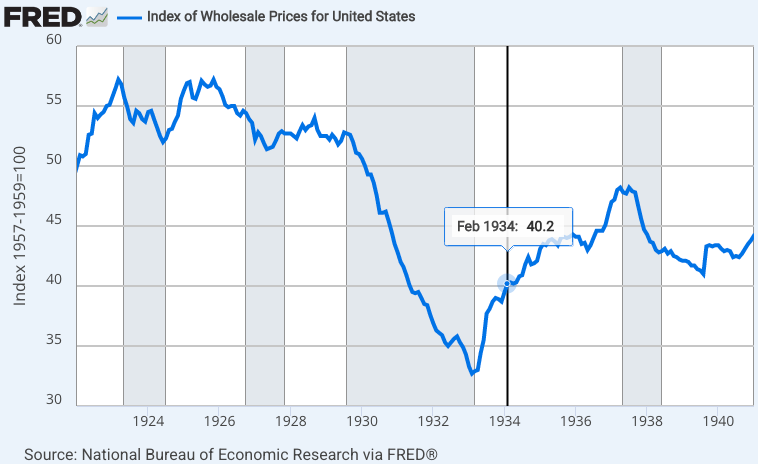

Long time readers probably know where I’m going with this, but to fully understand this quote it helps to have a bit of background information. The commodity-intensive Wholesale Price Index had fallen 38% from its July 1929 peak to its February 1933 trough. In his campaign, Roosevelt had publicly committed to restoring the price level back to 1926 levels. To accomplish this goal, FDR gradually depreciated the dollar by increasing the dollar price of gold. The policy attracted intense opposition from conservatives, and by late 1933 even liberals like Keynes were suggesting that he had gone too far. Over the objection of George Warren, in February 1934 FDR gave in and re-pegged the dollar to gold at a new price of $35/ounce.

So what’s going on with the Warren quote above? FDR had been sweet talked by his advisors into believing in those mythical “long and variable lags”, and that prices would soon recover to their pre-Depression levels. To be clear, the existence of sticky prices means that there are indeed some lags between monetary policy and broader price indices. But commodity prices respond almost immediately to economic policy shocks, and thus Warren understood that more stimulus was needed to fully reflate the economy.

The Wholesale Price Index is a mix of sticky final goods prices and flexible commodity price indices. FDR needed a more than 50% rise in the WPI in order to restore the pre-Depression price level. He didn’t even come close. The WPI soared by 23% between February 1933 and February 1934, but only another 7.2% over the next six years.

Warren understood that when it comes to monetary policy there is no “wait and see”. If the commodity markets are telling you that monetary policy is too tight to hit your policy target, then it’s too tight. Market prices respond immediately to changes in the stance of monetary policy. (As an aside, I don’t believe the pre-war price level was the right target.)

In mid-September 2008 (right after Lehman failed), the Fed thought that it had established a monetary policy that was expansionary enough to meet its policy goals. The Fed decided to keep its interest rate target unchanged at 2%. But the markets were clearly signaling that policy was too tight.

The September 2008 FOMC meeting radicalized me. Soon after, I began doing everything I could think of to get people to understand that money was too tight. George Warren’s lament about the abandonment of the dollar depreciation program shows that as far back as 1934, at least one economist looked at the world in a similar fashion.

People of today often look down upon previous generations. For instance, I’m currently watching Mad Men, a show that makes the people of 1960 look stupid. But that’s not how I recall the 1960s. The people of the 1960s would be horrified by the stupidity of our modern politicians.

In fact, previous generations often had a quite sophisticated understanding of economic events, even if they lacked our current models. Consider this NYT story from 1933, discussing the effect of changing the official government buying price of gold:

“The behavior of the foreign exchange market yesterday offered another illustration of the fact that the decline in the dollar is due not so much directly to the daily advances in the RFC’s gold price as to the government’s avowed intention of cheapening the dollar which these rises in the gold quotation indicate. Yesterday the RFC’s gold price was left unchanged from the previous day, but the market ignored the implication that the RFC was content for a moment not to push further the cheapening of the dollar. Instead it fastened its attention on the news of the changes in the Treasury Department’s administration, which it interpreted as still further reducing the influence of those opposed to drastic dollar depreciation.” (NYT, 11/16/33, p. 37.)

That’s a beautiful application of the rational expectations model, nearly 30 years before John Muth and 40 years before Robert Lucas. Gold prices increased on news that conservative opponents of devaluation were leaving the Treasury, even on a day where the administration did not formally raise the official buying price of gold. Indeed, FDR refrained from doing so on that particular day partly because he didn’t wish to further disturb markets already shaken by these resignations. Market participants were not just focusing on the government’s “concrete steps” (gold buying prices), they were looking beyond those actions, and reacting to changes in expectations of the entire future path of policy.

Even today, macroeconomists often ignore the implication of efficient markets. A wonderful 1937 quote from Paul Einzig shows that this has always been the case:

“On June 9, 1937, this veteran monetary expert [Cassel] published a blood-curdling article in the Daily Mail painting in the darkest colours the situation caused by the superabundance of gold and suggesting a cut in the price of gold to half-way between its present price and its old price as the only possible remedy. He took President Roosevelt sharply to task for having failed to foresee in January 1934 that the devaluation of the dollar by 41 per cent would lead to such a superabundance of gold. If, however, we look at Professor Cassel’s earlier writings, we find that he himself failed to foresee such developments, even at much later dates. We read in the July 1936 issue of the Quarterly Review of the Skandinaviska Kreditaktiebolaget the following remarks by Professor Cassel: ‘There seems to be a general idea that the recent rise in the output of gold has been on such a scale that we are now on the way towards a period of immense abundance of gold. This view can scarcely be correct.’ . . . Thus the learned Professor expected a mere politician to foresee something in January 1934 which he himself was incapable of foreseeing two and a half years later. In fact, it is doubtful whether he would have been capable of foreseeing it at all but for the advent of the gold scare, which, rightly or wrongly, made him see things he had not seen before. It was not the discovery of any new facts, nor even the weight of new scientific argument that converted him and his fellow-economists. It was the subconscious influence of the panic among gold hoarders, speculators, and other sub-men that suddenly opened the eyes of these supermen. This fact must have contributed in no slight degree towards lowering the prestige of economists and of economic science in the eyes of the lay public.” (1937, pp. 26-27.)

[You may want to inspect the graph above to better understand Einzig’s point. Prices briefly spiked in 1936-37 for reasons unrelated to the 1933 devaluation.]

Think of all the so-called experts who insisted that it was obvious that asset X was wildly overpriced at time=t, but at the same time held X in their 401k and took no steps to short the market. John Paulson became famous because he shorted the market in 2008. The fact that this action made him famous tells me all I need to know about all the people who claim they “saw it coming”. If you’re so smart how come you aren’t named John Paulson? I recall an ad for The Economist that bragged about how they had correctly called the housing bubble. But when I looked at their actual predictions, they were mostly far off base—most housing markets were higher than when they called the bubble. People still praise Greenspan for his 1996 claim that the stock market showed “irrational exuberance”, even though the claim turned out to be inaccurate. In retrospect, stock prices in 1996 seem quite reasonable—it was a great time to buy stocks. (You can debate 2000 prices, but not 1996.)

I found that by studying both economic history and the history of economic thought, I learned many macro insights that I would never have obtained by memorizing a few DSGE models in a graduate economics program. George Warren’s 1934 complaint turned out to be more accurate than the so-called “experts” of the day. My view that policy was too tight in September 2008 turned out to be more accurate than the Fed’s view, as even Ben Bernanke acknowledged in his memoir.

Students occasionally ask me what grad program they should attend. I cannot answer the question, other than to say you should look for grad programs that care more about ideas than equations.

PS. While reading an advance copy of George Selgin’s outstanding new book on the New Deal, I came across this passage:

Jacob Viner once told Roosevelt that he didn’t think “renewing his [Roosevelt’s] warfare against business” was a good idea (Fiorito and Nerozzi 2009, 17). “Viner,” Roosevelt said in reply, “you don’t understand my problem. If I’m going to succeed and if my administration is going to succeed, I have to maintain a strong hold on my public. In order to maintain a firm hold on the public I have to do something startling ever once in a while. I mustn’t let them take me for granted.”

Imagine having a president that liked to be the center of attention.

My suggestion is that you read chapters 1-6 of George’s book, then read The Midas Paradox, and then read chapters 8-26. :)

"Imagine having a president that liked to be the center of attention." These days, it's hard NOT to imagine that.

As Dr. William Barnett says: “the Fed should establish a “Bureau of Financial Statistics”.

For example, the monetary base should exclude its currency component. An increase in currency is contractionary, not expansionary.