I'm not budging

Bad ideas are still bad

It is often best to leave well enough alone.

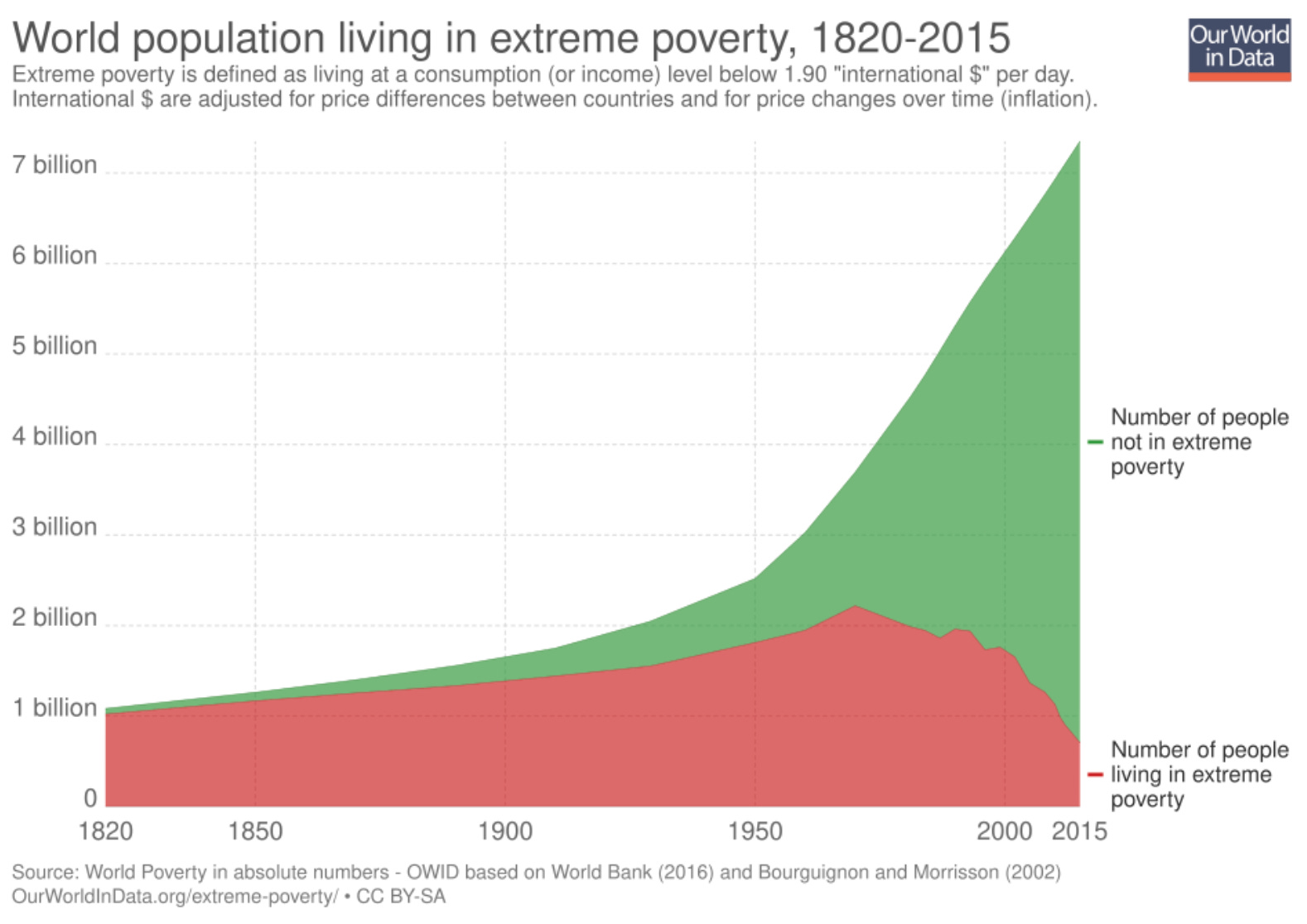

Throughout human history, there have been many golden ages. But there’s been none that were anywhere near as golden as the end of the second millennium. The world saw its greatest economic boom in the late 20th century, and this dramatically reduced the share of the population suffering from extreme poverty. The proximate cause of this boom was economic reforms in many countries, most notably China, India and Eastern Europe, but also including places such as Australia, New Zealand, Chile, Panama and the Dominican Republic. In terms of human welfare (and what else matters?) the neoliberal boom is by far the best thing that ever happened:

In my own field of economics, a “Washington Consensus” was reached that industrial policies do not work and that free market reforms were the way to go. Between 1990 and 2000, six Nobel Prizes in Economics went to professors at the University of Chicago, a hotbed of free market economics.

In the field of macroeconomics, things had never been better. The profession had largely moved away from outdated Keynesian ideas such as using fiscal policy to stabilize the business cycle, or the myth that monetary policy was ineffective at the zero lower bound. Western economists were highly critical of the Bank of Japan for not doing enough monetary stimulus to escape from deflation, dismissing BOJ claims that it was powerless to act. Fiscal austerity was in style, and indeed the US ran three consecutive budget surpluses at the end of the millennium.

Of course, things were not perfect. Although the famous “China Shock” paper argued that trade with China was beneficial to the US in an overall sense, the authors also showed that many local communities were adversely affected. Unfortunately, people cannot leave well enough along. Just when economic scholars and policymakers had mostly figured things out, we got restless and began reverting to all the mistakes of the mid-20th century. Here are just a few examples:

Economists began to doubt the efficacy of monetary policy, especially at the zero lower bound.

Economists began to forget about monetary offset of fiscal policy.

Economists began to suggest that budget deficits don’t matter when interest rates are low. (But what if they don’t stay low?)

Economists increasingly cited interest rates as an indicator of the stance of monetary policy. (They are not.)

Economists began edging back toward discredited Phillips Curve theories that favor easy money as a way to create jobs.

Economists found strange new respect for previously discredited policies such as price controls and protectionism, at least in limited cases.

Economists began to revert back to discredited theories that antitrust officials needed to worry about low prices, not high prices.

Some economists began to question whether the Fed was even able to target inflation, as various fiscal theories of the price level became popular on both the left and the right, despite almost no empirical support.

It is difficult to disentangle cause and effect. Did the changing views of economists cause a deterioration in public policy? Were opportunistic economists trying to cash in on a change in the prevailing sentiment of policymakers? Or were both responding to a change in the zeitgeist?

Whatever the explanation, we began to see more advocacy of policies such as government ownership of formerly private business, the increased use of rent controls, and Wright-Patman style anti-trust regulation. There was a rise in protectionism. After the mid-2010s, we implemented reckless and unsustainable fiscal deficits.

Unlike during previous periods of American history, this was mostly an unforced error. No world war or Great Depression made big deficits inevitable. We did this to ourselves.

It has become fashionable to reject neoliberalism, but the arguments against it are quite weak. In almost every case, the more neoliberal economy does better than the otherwise similar less neoliberal economy. Similarly, arguments against circa 2005 monetary theory are quite weak.

By the early 2000s, the Fed had adopted a very effective monetary regime, which kept inflation close to 2%. The Fed had a small balance sheet, with liabilities that were 98% composed of currency. The asset side of the balance sheet was almost entirely Treasury securities. And then in 2008 we threw it all away, with a completely unnecessary policy of paying interest on bank reserves. This led to a massively bloated Fed balance sheet, which allowed our central bank to intervene much more aggressively in the credit markets.

Call me a grouchy old reactionary, but I’m not budging. The policy consensus of 20 years ago was far superior to the policy consensus of today. In my view:

Fiat money central banks can always boost nominal GDP, if they choose to do so. They can also restrain inflation, if they choose to do so.

We should not pay interest on bank reserves.

We should not use fiscal stabilization policy.

We should balance the budget, at least in real terms.

We should have free trade with countries that don’t invade their neighbors.

Anti-trust should focus on high prices, not low prices.

We should avoid so-called industrial policies. (Check out Richard’s Hanania’s post on the subject.)

We should avoid rent controls, price controls and government ownership of business.

We should end residential zoning restrictions and move toward school choice, health saving accounts, carbon taxes, congestion pricing and progressive consumption taxes.

At the end of the last millennium the world had finally figured it out, and then . . .

To answer your rhetorical question about what else matters besides human welfare: animal welfare, potentially. Global livestock populations exploded alongside the neoliberal boom. If you’re doing utilitarian math and animals have any nonzero moral weight, the scale of factory farming (80+ billion land animals slaughtered annually, most in conditions that would be criminal if done to dogs) might swamp the human welfare gains.

We are getting rent control by the back door here in the UK. Surely this time it will work?