No “wait and see”

Using markets to evaluate public policies

Richard Hanania has an interesting post explaining why it is often a mistake to take a wait and see approach to judging public policies:

In the weeks after Maduro was seized, the value of the Venezuelan stock market skyrocketed 260%. Some argue that liquidity was low, but tens of billions of dollars isn’t exactly nothing, and I put a lot of weight on this piece of data. In The Midas Paradox, Scott Sumner judges the wisdom of US policy up to and throughout the Great Depression based on the immediate movements of the stock market, and other indicators like bond and foreign exchange markets. If FDR announced a change in policy and the stock market went down, for example, he doesn’t care if it ended up rising six months down the line. The theory behind this idea is that people with skin in the game take into account all foreseeable circumstances at the time an event occurs, and what happens later can always be better explained by more proximate causes. I prefer this approach because otherwise you can just come up with any story you want about the wisdom of various economic policies.

I’m not really a fan of the Maduro raid, for “rules utilitarian” reasons that I discuss in a post that I wrote a few weeks ago but haven’t gotten around to publishing yet. But I do believe that Hanania is correct that the raid is a net positive for Venezuela and indeed may well end up being a positive for the US as well. (Hanania also discusses the negative market response to the Iran War.) Because Hanania cites my previous work in this area, I thought I should do a post explaining my views.

I’ve often argued that there is no point in waiting to see what happens after policies are adopted that have the goal of influencing aggregate demand. Thus, when the Fed makes a major policy announcement, we know within minutes everything we will ever know about the impact of that action. Because this claim is so unconventional—and would likely be rejected by most economists—I’d like to defend the idea using an analogy from the world of sports.

Assume that the Las Vegas betting line has the Kansas City Chiefs a 10-point favorite over the Tennessee Titans. Two days before the game, Patrick Mahomes is injured in practice, and the betting line drops to KC by two points. In the actual game, the Chiefs end up winning by 11. How should we think about the impact of the injury to Mahomes.

[www.allproreels.com — Washington Football Team vs. Kansas City Chiefs from FedEx Field, Landover, Maryland, October 17th, 2021 (All-Pro Reels Photography)]

Those who favor a “wait and see” approach, might argue that the injury had no impact, as the Chiefs actually won by more than the pre-injury line. I would argue that the injury reduced the Chiefs expected net performance by 8 points, as prediction markets are the best way of ascertaining the truth about reality. The actual outcome of any game is highly unpredictable, as it is influenced by a wide range of factors that are difficult to forecast. Even the shape of the American football adds randomness to the game, as it often bounces unpredictably during punts.

Most economists are fairly rational thinkers, and I suspect that most of them would agree with my claim about point spreads in a Chiefs game. The betting line provides more accurate information about the impact of an injury than the actual outcome of the game.

But I also suspect that most economists disagree with my rejection of the wait and see approach to economic policy initiatives, and especially my claim that within minutes of a policy announcement we know everything we will ever know about the impact of the policy. Indeed, even I regard this claim as a slight overstatement, as Fed announcements include more than a rate change, and there is often further market reaction during the afternoon of a Fed announcement, as markets digest both the forward guidance in the full statement and also the interpretation provided by pundits. Even so, the market reaction is mostly complete by the end of the trading day.

In January 2001 and again in September 2007, markets responded very positively to more expansionary than expected Fed announcements, and in December 2007 the response was very negative to a more contractionary than expected announcement. You could argue that only the latter reaction was ”correct”, as in all three cases we eventually went into recession. But I don’t see it that way. Rather, in all three cases the markets were worried about recession, and in all three cases they were “rooting” for actions that made recession less likely.

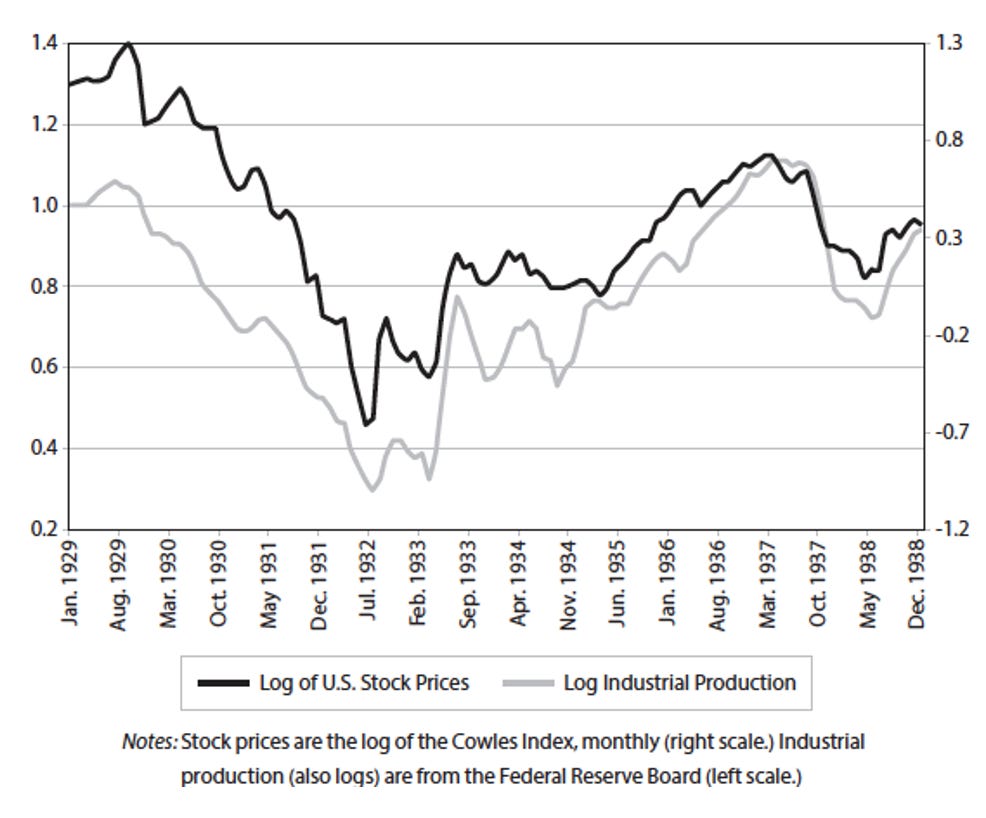

As Hanania indicated, in The Midas Paradox I spent a lot of time looking at stock market reactions to policy shocks. To be clear, I do not believe that the stock market is a reliable indicator in all circumstances. To take an obvious example, I would not use the stock market reaction to a cut in corporate tax rates as a indicator of whether lower corporate taxes were good public policy. So why did I frequently use them when evaluating policy during the Great Depression?

A graph in The Midas Paradox shows an unusually strong correlation between (logs of) stock prices and industrial production from January 1929 through December 1938:

(Notice the lack of “long and variable lags”.)

The term ‘ad hoc’ is often seen as a pejorative, but when special circumstances allow a technique to be unusually effective, then it makes sense to use that technique. It just so happens that output was undesirably low throughout the entire 1930s. It is also the case (probably for related reasons) that stock prices and industrial production were unusually closely correlated during this period. In that economic environment, policies that tended to raise output also tended to raise stock prices, and vice versa. The same might not be true in an overheated economy such as 2022-23. And even in the 1930s, I did not rely solely on stock prices. I also looked at the reaction of numerous other financial market indicators, including bond yields, yield spreads, exchange rates, and commodity price indices.

I got into blogging out of frustration that the Fed seemed to ignore market signals in late 2008. For instance, it refused to cut rates in the meeting after Lehman failed, despite plunging TIPS spreads. Readers often tell me that they like my blog because my takes have been more accurate than those of many other pundits. While some warned that Bernanke’s QE would create high inflation, I predicted that inflation would remain below target. While Keynesians predicted that fiscal austerity would sharply slow the economy in 2013, the economy actually accelerated.

Alex Tabarrok also thought the 2013 “market monetarist experiment” was a bad look for Keynesians, although he rightly noted that a single experiment is not decisive. My relative complacency about the fiscal austerity was mostly based on the relative stability of various asset prices, including stocks and TIPS spreads. I didn’t have a high level of confidence that we market monetarists would “win” this contest, but then it was the market forecasts that mattered to me, not the subsequent real-world outcome. Unfortunately, the world I live in doesn’t agree with me, and I’m forced to play by their rules—the “wait and see” approach. Luckily, in 2013 I came out ahead. But even if I had been wrong, I would not have regretted relying on market signals.

I'm certainly no Nostradamus. When the markets are wrong (and they are frequently wrong), then I’m also wrong. Unlike in 2013, I would have lost a bet made in 2021 on whether the fiscal and monetary stimulus would lead to high inflation. If you bet on a series of football games with the point spread in your favor, you will usually win. But losses will by no means be infrequent. The rationalist community argues that the best we can hope for is to be “less wrong”, and I believe that market forecasts are the best way of doing that.

I was a relatively unknown economist in 2008, teaching at a second-tier college. Whatever reputation I have comes from my use of market signals in blog posts. Because I’m not good with technology, I didn’t get my blog up and running until early 2009. If I’d started blogging in mid-2008, my reputation might be somewhat higher. But I have no reason to complain. If I’d started blogging in 2005 my reputation would be far lower, as I deny the existence of bubbles, including housing bubbles. I still don’t believe that 2006 was a bubble (real housing prices have since recovered), but most people don’t see things that way.

While I approve of Hanania’s general approach to evaluating the success of policy initiatives, let me end with a note of caution. Markets are not very good at evaluating existential risks. Consider a hypothetical foreign policy initiative that increases the risk of a major nuclear war by 1%. Perhaps a US decision to go to war with Russia over Ukraine, or China over Taiwan. Also assume that a nuclear exchange would kill 200 million people. How would markets react to that risky policy initiative?

Even if nuclear war drove US equity prices down close to zero, the stock market might only decline by 1% on the news of US intervention, as the risk of nuclear war has increased, by assumption, by only 1 percent. But even a 1% risk of nuclear war has an expected value of 2 million deaths and thus is very likely a bad policy choice.

I’m not certain if the Munich agreement of 1938 slightly increased the chance of a war that ended up killing 50 million people, but this New York Times report has always haunted me:

From a strictly market viewpoint the news of the decision of the Czech Government to capitulate to the demands that it cede the Sudeten area to Germany was favorable. Prices, quite naturally, improved as the threat of war seemed to recede. But this was “good news” with a difference; hardly the sort of good news to capture the imagination of individual traders and evoke a spirit of bullishness. Even in Wall Street, where the mental processes are supposed to be exceedingly realistic, there was a sufficiently powerful sense of the tragedy involved in Czechoslovakia’s surrender and the unhappy role that Britain and France played in bringing it about to dampen the normal speculative impulses. (NYT, 9/22/38, p. 33)

I suspect that the US stock market might rise if Trump were to pressure Ukraine into surrendering to Russia, or even ceding the Sudetenland . . . er . . . I mean the Donbas. Call me a hypocrite, but I worry about the tail risk of appeasing Putin.

Another problem is that events can be ambiguous. Does the failure of oil to hit $150/barrel mean the war doesn’t matter all that much, or does it incorporate market expectations of a “Trump put”, an expectation that he would back off if the global energy outlook became extremely bad?

PS. What do you think of the NYT’s writing style back in 1938? It is obviously different from today, but I feel like someone else could evaluate that difference better than I can. Do you like it better or worse? Is it aimed at a more elite audience? Or is it simply more “literary”?

PPS. Tyler Cowen had this to say today:

On the precautionary side, we need a dash of the 1960s and ’70s New Left and libertarian anti-war ideologies, skeptical of Uncle Sam himself. We do not want to become the bad guys.

Yup.

I don’t think the only issue in the trump case is that outcomes are ambiguous, its that prices are endogenous. The price of the DOW has an impact on how trump acts, so you don’t know what a price change means.

Example: trump passes a 100% tariff tomorrow, stocks fall by 8%. Does this mean the policy only impacted valuations by 8%? No, it means that people are afraid to sell in case their selling causes the tariffs to be rescinded.

I sort of agree with your position in principle but I think there are a lot of caveats.

One important one: what if the policy / event is communicating some information, markets could adjust based on the information rather than the policy event. For example suppose there are two related policies A and B, and markets are unsure if this general family of policies will be pursued. When policy A is enacted, they may react based on changing views on the chance of B being enacted as well, even if A is unimportant itself.

Maybe a country is more likely to declare war on another country if it feels good about its military prospects, so on the declaration of war markets adjust not just based on the actual policy of war, but also the private information about military capacity being revealed by the decision.