The eternal quarter

Why tariffs won't cause much inflation (but are still bad)

During the 19th century, the US had roughly zero inflation, on average, despite some fairly high tariffs. Indeed the “cost of living” in 1933 was still about the same as when the country was founded in 1776. Does this surprise you? It shouldn’t. In this post I’ll explain why the Trump tariffs are not likely to be very inflationary, but nonetheless will be bad for the economy.

Consider the following two claims:

Claim #1:

In 1925, a quarter could purchase about 5 quarts of gasoline.

Today, a quarter can purchase barely a cup of gasoline (at $4.16/gallon).

Claim #2:

In 1925, a quarter could purchase about 5 quarts of gasoline.

Today, that same quarter can still purchase about 5 quarts of gasoline.

Both claims are true, at least here in California. Back in 1925, gasoline cost about 20 cents per gallon. So a quarter could buy about 5 quarts of gas.

The 1925 quarter contains 0.18 troy ounces of silver. So when silver is selling for $30/oz., the old quarter contains $5.40 worth of silver. This means a 1925 quarter can purchase still roughly five quarts of gasoline (assuming the current dollar price of gas is $4.32.)

You might think that both silver and gasoline have become much more valuable since 1925. But that’s just a cognitive illusion, or perhaps you could call it the money illusion. In reality, it is fiat money that has become much less valuable.

Today, we are so used to a persistently rising cost of living that people are surprised to hear about the relative lack of inflation prior to 1933. They are surprised that persistent inflation only applies to post-1964 (copper/nickel) quarters, not pre-1964 (silver) quarters. And yet there’s nothing unusual about the old quarters, it’s the new ones that are weird.

Nominal price changes reflect a change in the value of one asset (gasoline) in terms of another (money). Ex ante, it’s not obvious why you’d expect the value of any given asset to rise or fall over time. It would depend on the supply and demand dynamics in the market for silver and for gasoline. That’s why with commodity money standards (usually silver or gold), the average rate of inflation was roughly zero, although there can be short-term volatility, as with the relative price of any two commodities.

Thus it is the recent persistent inflation that is odd, not the ups and downs of prices from 1776 to 1933. The cost of living rose somewhat after we devalued gold in 1933, but really took off when we removed silver from money in 1964 and stopped pegging gold at $35/oz. in 1968.

But even paper (fiat) money is not necessarily inflationary. It has turned out to be inflationary in the US, but fiat money in Japan and Switzerland has not been particularly inflationary during recent decades. It depends on monetary policy:

Central bankers are a bit like old generals, always fighting the last war. In 2021, they tried to avoid repeating the disinflationary mistake of the early 2010s, and today they are likely to be vigilant against a repeat of the inflationary mistake of 2021-22. In addition, I suspect they have a fairly low opinion of Trump’s tariff policy, and are not likely to bend over backward to “bail him out.” After all, they’re only human.

To be clear, I believe the Fed will (and should) allow tariffs to result in roughly another percentage point in inflation for a year or so, but that’s probably all. The bigger threat is the risk that our reckless fiscal policy (a far worse mistake than Trump’s tariff policy) will eventually cause the previously false fiscal theory of the price level to eventually become true. That is, there is a risk that the Fed will eventually be pressured to monetize the debt. We’re not there yet, but it is a long-term risk.

So what do old quarters have to do with the risk of tariffs causing inflation? Think about all of the explanations that people offer for inflation:

Greedy unions. (You heard this more in the 1960s and 70s than today.)

Greedy corporations.

Big budget deficits.

Supply shocks.

Tariffs

If those explanations actually were true, then you’d have expected the 1925 quarter to have lost much of its purchasing power over the past century. But it hasn’t, not at all. That’s because inflation isn’t really about goods prices, it’s about the value of one specific asset—money. We will have inflation if and only if the Fed allows the purchasing power of base money to decline. They have a 100% monopoly on the supply of base money, which is all the power they need. But since 2008, they have added an additional policy tool, interest on bank reserves, which gives them substantial control over the demand for base money. The price level is determined by the Fed, plus or minus a few short run perturbations due to misjudgments.

Part 2: The impact of tariffs

So if tariffs don’t cause very much inflation, does that mean they aren’t very bad? No, in an absolute sense tariffs are a quite distortionary economic policy. But relative to the almost unimaginably large size of the economy, they are not likely to be a major factor—at least at currently proposed levels. As an analogy, the moon is a long way away in absolute terms, but is close by to Earth relative to other planets and stars.

I have occasionally cited Singapore as the most free market economy in the world, according to various rankings. When I do so, a very persistent troll invariably points to a few Singaporean policies that are interventionist. What he fails to understand is that all economies are riddled with government interventions. In the US, we have tens of thousands of regulations, barriers to entry, price controls, tariffs, quotas, government-owned industries, subsidies, distortionary taxes, etc., etc. It’s difficult to find a single American industry that is not significantly distorted by various sorts of government intervention. Perhaps the dry cleaning industry is a fairly free market.

Americans often complain that Europe is too “socialist”, or that China is too “communist”. But even America’s supposedly pro-capitalist political party doesn’t actually believe in free markets. Hardly a day goes by without some new GOP initiative to ban lab grown meat, or to restrict wind energy, or to put price controls on drugs, or to enact huge subsidies for farmers, or to put tariffs on imports, or to enact Nimby regulations on homebuilding, or to make the tax code far more complex in a way that helps GOP friendly industries and hurts Democratic friendly industries. In other words:

There is a great deal of ruin in a nation.

Protectionists often point to the fact that the US successfully industrialized during a period of fairly high tariffs. But why focus on that one policy? It’s also true that America industrialized during a period of open borders. And a period with no central bank. And a period with no income tax. And a period where cocaine and heroin were legal. And a period with Jim Crow laws. And a period where women couldn’t vote. Lots of good and bad things are happening all the time.

Tariffs are bad, but the budget now going through Congress looks to be much worse. It will likely be the single most reckless fiscal bill in all of American history. (BTW, we often ran surpluses in the late 1800s. I don’t see the protectionists advocating that policy—even though it would be far more effective than tariffs at boosting manufacturing.)

Unfortunately, what I’ve been warning about over the past decade is now coming true. I started warning about the fiscal situation back in the late 2010s, when many other bloggers suggested that fiscal hawks like me were out of touch, that we were old fogies that didn’t understand we were now in an MMT world of free money. Yes, interest rates were low for a while, but we didn’t pay off those debts, and they are now being rolled over at much higher rates.

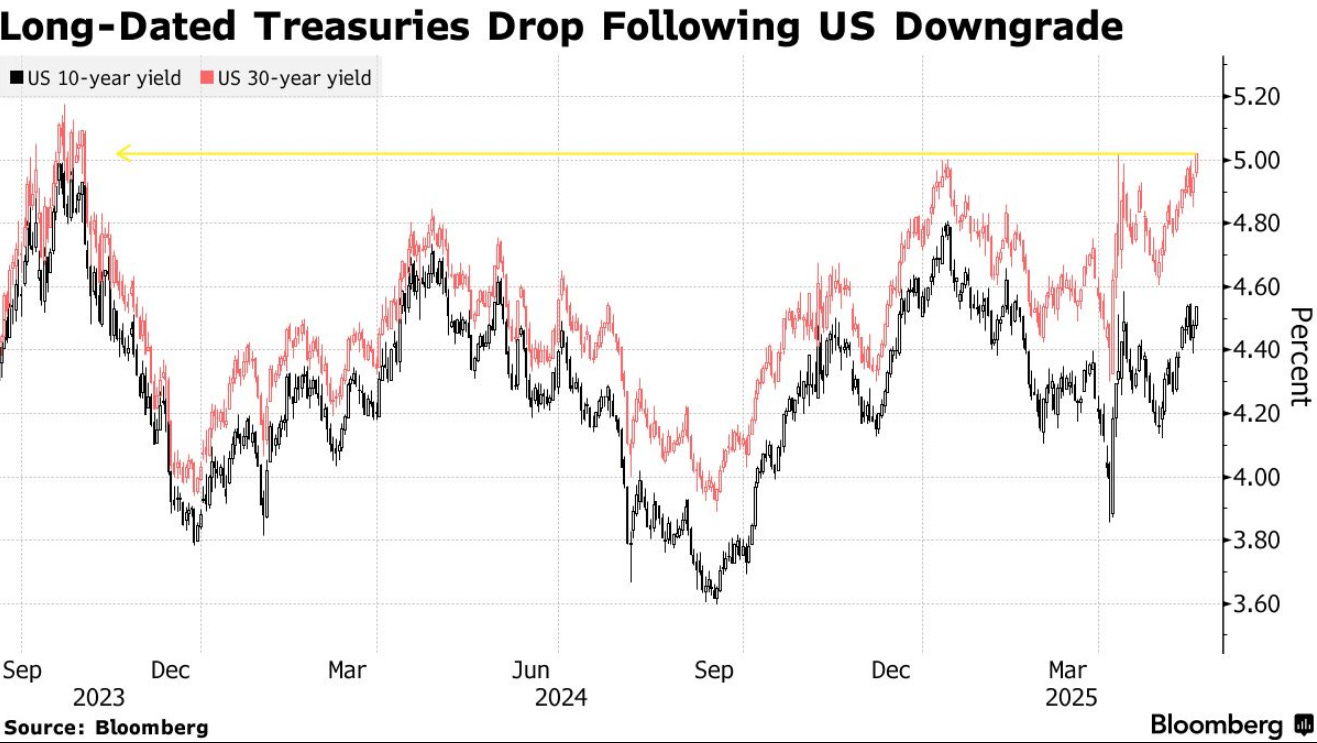

I cannot be certain, but I suspect the widening spread in this Bloomberg graph partly reflects worries over the long run fiscal situation:

PS. You may recall that I predicted that China was in the stronger negotiating position that the US. Fortunately, that turned out to be true. Here’s Bloomberg:

China’s defiant stance in negotiating a tariff truce with the US has convinced some countries they need to take a tougher position in their own trade talks with the Trump administration. . . .

US President Donald Trump’s willingness to retreat so much from the earlier 145% duty on China surprised governments from Seoul to Brussels that have so far stuck with the US’s request to negotiate rather than retaliate against its tariffs.

After China’s tough negotiating tactics earned it a favorable — albeit temporary — deal, nations taking a more diplomatic and expedited approach are questioning whether that’s the right path.

“This shifts the negotiating dynamic,” said Stephen Olson, a former US trade negotiator who’s now a visiting senior fellow with ISEAS — Yusof Ishak Institute in Singapore. “Many countries will look at the outcome of the Geneva negotiations and conclude that Trump has begun to realize that he has overplayed his hand.”

I hope other countries stand up to the US. I’d love to see our government retreat like a dog with its tail between its legs.

PPS. The original Standing Liberty Quarter showed an exposed breast, but this was covered up during mid-1917. I had always assumed that was done because of complaints by prudish Americans. While researching this post I discovered the actual reason was probably the US entry into WWI in April 1917. Here’s Wikipedia:

The redesign of the obverse has led to an enduring myth that the breast was covered up out of prudishness, or in response to public outcry. Breen stated that "through their Society for the Suppression of Vice, the guardians of prudery at once began exerting political pressure on the Treasury Department to revoke authorization for these 'immoral' coins". Ron Guth and Jeff Garrett, in their book on US coins by type, aver that the covering up of Liberty was "a change never authorized by MacNeil". Numismatic historian David Lange concedes that there is no evidence of outcry from the public, but suggests that the decision to change the coin was "more likely prompted by objections from the Treasury Department". Numismatist Ray Young, in his 1979 article in Coins magazine about the quarter, suggested that the redesign "came from the symbolism. If Liberty was going to stand up to her foes, she should do so fully-protected—not 'naked to her enemies.' Thus the war probably had much more to do with the change than any alleged 'public indignation.' "

Here’s the original version:

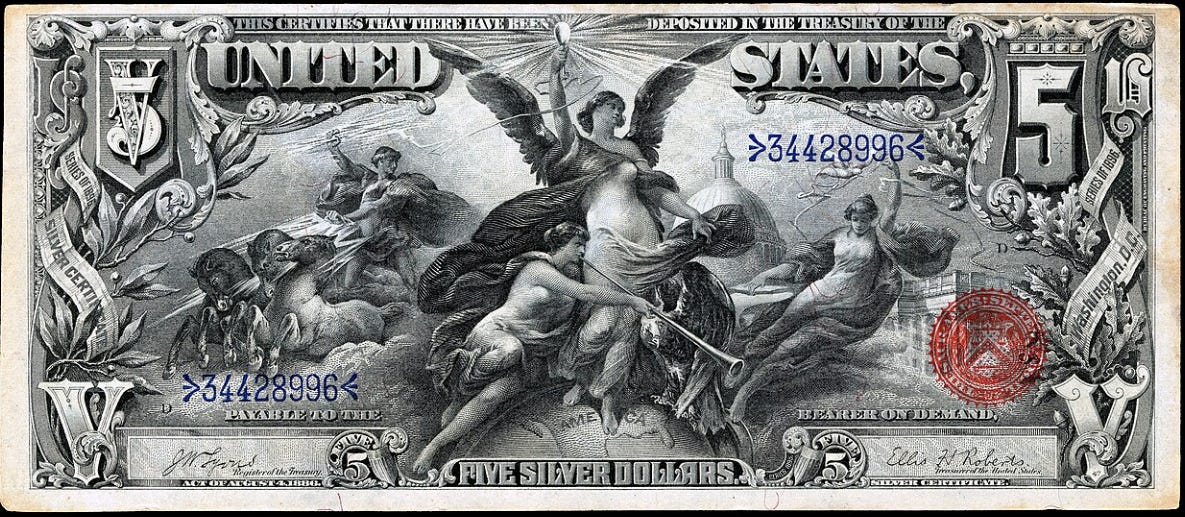

However, I do believe that the American public has recently become more prudish. I wonder if this $5 currency note (from 1896) would be acceptable today:

> However, I do believe that the American public has recently become more prudish.

Professor Harold Bloom, during a talk on this book "How to Read", recited Sonnet 121, and described it as "the most powerful expression in the language of being condemned for erotic activity by the false adulterate eyes of others, who themselves be beveled, that is to say crooked. And I wish the poem could be read aloud frequently on television during our recent national orgy of virtue alarmed as manifested by talking heads and congressmen".

This was at the height of the Clinton impeachment. Whether or not the public has become more prudish, there is greater pious prudishness-signaling among talking heads.

This is all fair, and I agree. But a few weeks ago you appended a post with "As I keep saying, late 20th century neoliberalism is the best thing that ever happened" and referred to a graph showing a sharp decline in the fraction of people living in extreme poverty since the 1950s or so. But lots of things besides neoliberalism have been going on since the late 1900s, including nuclear proliferation, the invention of the internet, and major advances in medicine. It cuts both ways, Sumner.