China's mysterious deflation

China's mysterious deflation

China as the new Japan

Yes, I’m being a bit sarcastic, as there’s nothing at all mysterious about China’s current deflation. It is caused by a relatively tight monetary policy—full stop.

But there are some interesting mysteries that do need to be examined. Why don’t people understand that tight money is the problem? Why is China repeating the mistakes made by Japan during the 1990s? What are the political constraints faced by the Chinese central bank (PBoC)?

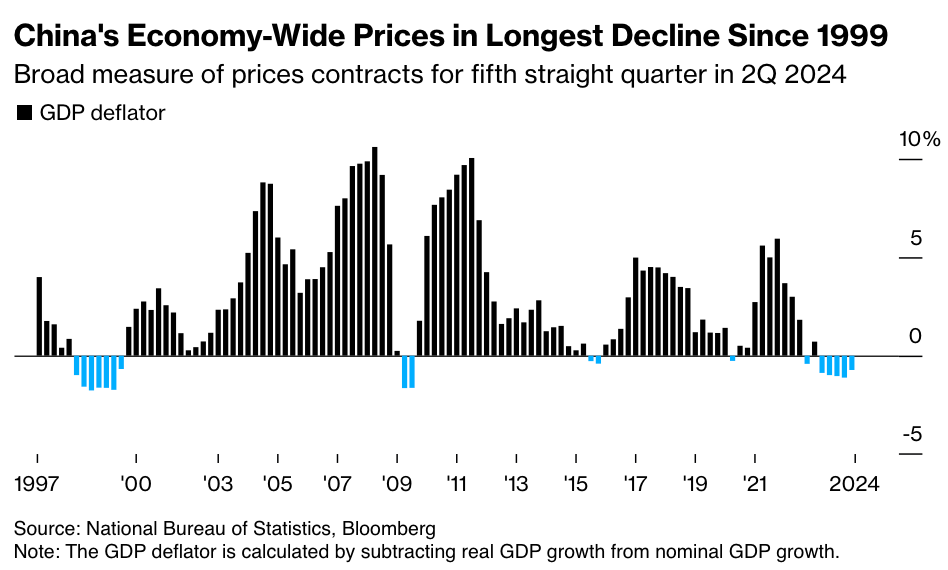

Bloomberg has an article that provides extensive discussion of the situation. Nowhere do they suggest tight money is causing the deflation, or that easier money might be a solution. As is frequently the case, the underlying problem is a misunderstanding of the fundamental nature of monetary policy. People view monetary policy as being in some sense about interest rates and the credit markets, whereas in fact it is all about the supply and demand for base money and the growth rate of nominal GDP.

To their credit, Bloomberg does at least recognize that a key problem is slow NGDP growth:

The weak price pressures are evident in the growth pace of China’s nominal GDP, which expanded just 4% in the second quarter — well under the nation’s real economic growth goal of around 5% this year.

At times of weak price gains, nominal expansion is a more useful indicator because it better reflects changes in wages, profits and government revenue, Luo Zhiheng, chief economist at Yuekai Securities Co., wrote in a note earlier this month.

Unfortunately, they fail to see the connection between slow NGDP growth and an excessively tight monetary policy.

This comment also caught my eye:

The dilemma is that even monetary expansion in China could be deflationary by being mainly directed at the supply side of the economy, Michael Pettis, a senior fellow at the Carnegie Endowment for International Peace, wrote in an article last month.

If you follow the link, Pettis is clearly talking about credit policy. He worries that China doesn’t need more credit expansion, as it already has substantial industrial overcapacity. I’m no expert on Chinese credit policy, but it is important not to conflate credit policy and monetary policy, they are two radically different concepts. If Pettis is correct about the credit situation, then China needs both a more contractionary credit policy and a more expansionary monetary policy.

If China is currently over-investing, then it means they simultaneously need both more NGDP and less investment. And as the Japanese learned in the 1990s and 2000s, even a recklessly expansionary fiscal policy doesn’t deliver more NGDP. Instead, Japan’s NGDP only began rising after 2012, when Japan switched to a tighter fiscal policy and a more expansionary monetary policy.

The Chinese government has many fiscal and regulatory tools to address the related areas of banking, credit and investment. Monetary policy is far too blunt an instrument to address sectoral imbalances. But it is the perfect tool to create more NGDP. Pettis suggests that Chinese monetary policy is set up in such a way that monetary expansion automatically triggers credit expansion. If so, then they need to change that policy approach, and do it soon.

A similar confusion occurs with real and nominal exchange rates. One of the root causes of the Japanese deflation was a reluctance to devalue the yen, which (in nominal terms) was clearly overvalued during the late 1990s. But Japan was running a large trade surplus at the time, which led some pundits to view the yen as undervalued. They were making the common mistake of conflating real and nominal exchange rates.

Current account surpluses occur when countries save more than they invest. In the long run, this has nothing to do with monetary policy, NGDP, or nominal exchange rates. Instead, the excess saving depreciates the real exchange rate, creating the trade surplus. When that occurs, anyone suggesting that Japan needs to depreciate its nominal exchange rate is likely to face comments such as: “How can you say they need to devalue, when they already have a huge trade surplus?” During the 1990s and 2000s, the US government pressured Japan to avoid currency depreciation, and this was one of the root causes of the Japanese deflation.

I do not know if a similar situation exists today in China. Is the Chinese government reluctant to reduce the nominal value of the yuan for fear of triggering trade retaliation? Is it worried about dollar denominated debts? Or is there confusion over the distinction between nominal and real exchange rates? As with Japan in the 1990s, it seems implausible that the renminbi needs to be weaker at a time when China has a large trade surplus. But even if China should have a stronger real exchange rate, it also needs a weaker nominal exchange rate.

Not surprisingly, the press also sees comparisons with Japan:

“We are definitely in deflation and probably going through the second stage of deflation,” said Robin Xing, chief China economist at Morgan Stanley, citing evidence from wage decreases. “Experience from Japan suggests that the longer deflation drags on, the more stimulus China will eventually need to break the debt-deflation challenge.”

That seems right. So why is China repeating Japan’s mistakes? What is the common thread that links these two big East Asian economies? One clue can be found by looking at a past example of Chinese deflation, from the late 1990s:

Does that date ring a bell? That’s right, China experienced a significant deflation in the late 1990s at exactly the same time as did Japan. Before identifying the common thread, let’s consider all of the explanations that do not apply:

China did not have a demographic crisis in the late 1990s, as its population was still rising briskly.

China was not overbuilt; indeed they still had a enormous need for investment to build up their economy.

China was not stuck in secular stagnation, indeed its real GDP rose rapidly during the 1990s.

As is often the case, the real problem was nominal. China’s monetary policy was increasingly contractionary, which explains why its NGDP grew more slowly than RGDP. You didn’t hear nearly as much about the Chinese deflation as the Japanese deflation, for reasons nicely explained by George Selgin in Less Than Zero. Deflation that occurs during a period of strong NGDP growth is not necessarily a problem.

Although the Chinese deflation didn’t do much harm, on balance they probably would have preferred a bit stronger NGDP growth. So why did the Chinese government adopt an increasingly contractionary monetary policy during the late 1990s?

The issue seems to have been the exchange rate. At the time, the yuan was pegged to the dollar at a fixed rate. When much of the rest of East Asia devalued after Thailand’s financial crisis, China (and Hong Kong) held firm. Thus, in relative terms their currency appreciated. Hong Kong also experienced deflation at the same time. So did Argentina (under its currency board.) When (demand-side) deflation occurs, the proximate cause is generally tight money and the root cause is frequently exchange rate policy.

Now we can see one important similarity between China and Japan—both are very large economies, where the exchange rate is a major foreign policy concern of other trading nations. Singapore uses its exchange rate as a monetary policy tool, and also runs a huge current account surplus. Because Singapore is small, however, other countries tend to ignore its surplus. Both China and Japan are much more in the spotlight.

Although China seems to be following in the footsteps of Japan, it has not yet hit the zero lower bound. But if you look further down the road, it is hard to imagine that China will be able to avoid a dramatic reduction in its natural (equilibrium) real interest rate. Its population has already started falling and its huge build out of housing and infrastructure must surely begin to taper off before too long. When that occurs, the PBoC will need to figure out how to operate in a low real interest rate environment.

The good news is that purely nominal problems are really easy to solve, if you have a correct understanding of the issue and deal with it in an effective way. A good place to start is NGDP level targeting. In the unlikely event that any PBoC officials read this blog, I’d suggest they take a look at my paper on the Princeton School of monetary policy, reprinted as chapter 3 of my book entitled Alternative Approaches to Monetary Policy. It provides a roadmap for operating at the zero lower bound.

Update (9/11/2024): Today’s Bloomberg added some important perspective:

“The China and Hong Kong investors I know are so disappointed, they are cutting down their already low exposure, feeling hopeless,” said Steven Leung, executive director at UOB Kay Hian Hong Kong Ltd, who’s been covering the market for 30 years. “Quantitative easing-type government liquidity is the only way out.” . . .

The People’s Bank of China is wary of cutting interest rates aggressively and further widening the gap with US rates, which would add depreciation pressure on the yuan. President Xi’s focus on the quality of growth has also seen Chinese officials hold off on aggressive stimulus moves. After a deleveraging push to deflate a property bubble led to the current crisis and scores of defaults among developers, authorities are reluctant to dramatically shift tack lest it builds up unwanted leverage.

Stephen Kirchner has a post on the same subject, which is far more informative than this post. Here’s an excerpt:

The very subdued price growth in the domestic economy, in contrast to the rest of the world, largely reflects China importing monetary conditions from the US via its managed exchange rate. It is ironic that for all of Xi’s focus on economic self-sufficiency and suspicion of foreign economic influence, China’s economy remains hostage to the US Fed.

Please read the whole thing

Everyone, I added a few updates at the end of the post. I highly recommend the Stephen Kirchner post that I linked to.

Central bankers cannot be left in charge of monetary policy. Inevitably they fixate on exchange rates or inflation too much.

The Bank of Thailand is also too tight. The Bank of Japan is barely accommodative enough, and yet it seems to want to become too tight. The Fed is likely too tight presently.

The macroeconomics profession is a muddle on what is QE, when concurrent to fiscal deficits. Michael Woodford says QE+deficits is money-financed fiscal programs.

John Cochrane just wrote a bunch of posts that Japan had the perfect monetary policy for decades.

If you are not confused, then maybe you do not understand the situation.