Good things are good

No, overproduction did not cause the Great Depression

Before examining a recent paper by Citrini and Alap Shaw on the impact of AI on the economy, I’d like to briefly review a popular misconception about the Great Depression—the view that the underlying problem was “overproduction”.

During the early 1930s, real output in the US declined by more that 30%. To give you a sense of the magnitude of this slump, recall that output only declined about 4% during the Great Recession of 2008-09. Given those facts, you might be surprised by the number of people that blamed overproduction for the Great Depression. What were they thinking?

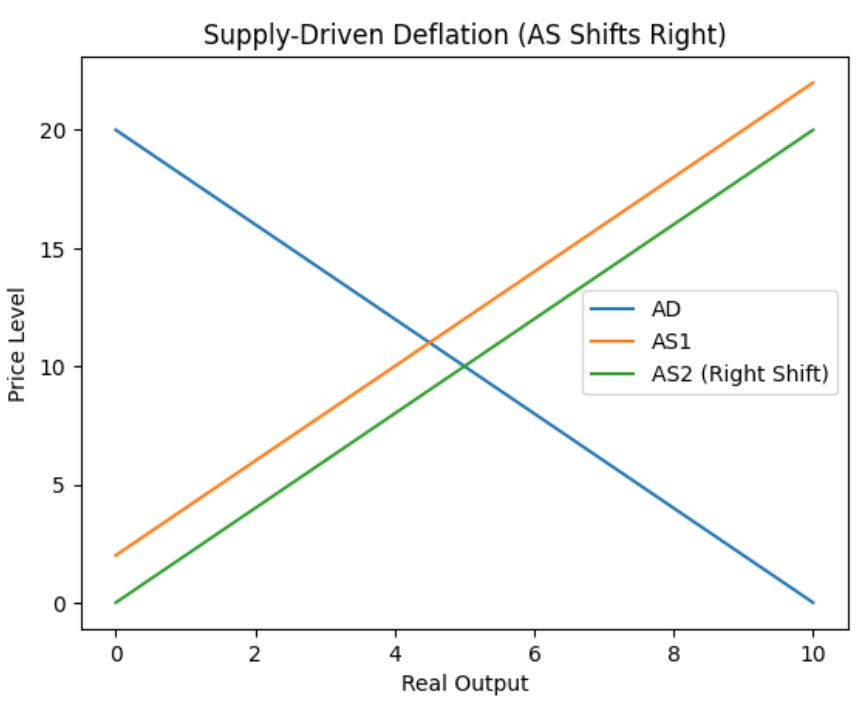

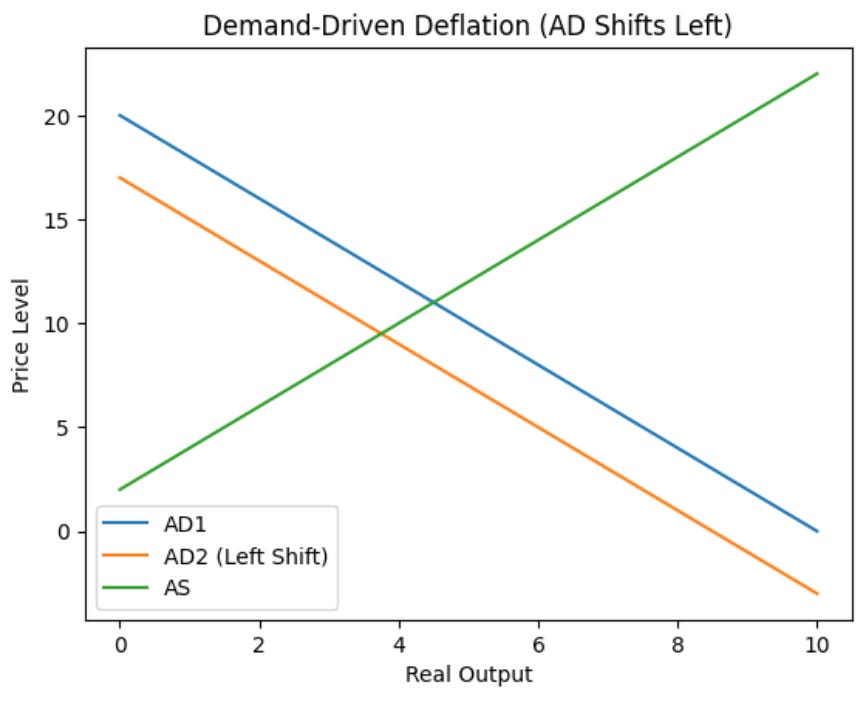

The contraction of 1929-33 didn’t merely see falling output, the price level also declined by roughly 25%. Franklin Roosevelt thought the deflation was making the Depression worse and believed that overproduction was the cause of the deflation. He got Congress to enact policies such as the National Industrial Recovery Act and the Agricultural Assistance Act, aimed at reducing production. He “succeeded”, as industrial production declined between July 1933 (when the labor codes were enacted) and May 1935 (when the NIRA was ruled unconstitutional.) Every so often the Supreme Court does a favor to economically illiterate presidents.

Even economists that were generally supportive of FDR, notably John Maynard Keynes, worried that the NIRA slowed the recovery. This is from a letter that Keynes wrote to FDR:

That is my first reflection--that N.I.R.A., which is essentially Reform and probably impedes Recovery, has been put across too hastily, in the false guise of being part of the technique of Recovery.

Long time readers know what I’ll say next. FDR’s view was a classic example of the fallacy of reasoning from a price change. FDR assumed that the deflation was caused by too much supply:

. . . whereas it was actually caused by too little demand:

I found the Citrini essay difficult to interpret, as they don’t use standard economic concepts in a conventional fashion. Here’s Brian Albrecht:

Right at the start, Citrini introduces a concept called “Ghost GDP”: output that “shows up in the national accounts but never circulates through the real economy.”

Ummm… yea, that’s not a thing.

GDP is not a number someone estimates and hopes is roughly right. I mean they do estimate it, but that’s not what matters here. It’s an accounting identity. Every dollar of output is, by definition, a dollar of income to someone. There is no output that “doesn’t circulate.” If a GPU cluster in North Dakota does the work of 10,000 white-collar workers, someone owns that output. Someone earned that revenue. The money went somewhere.

Where does the money go? That’s the question Citrini never asks.

The parts of the Citrini paper that I do understand are often wrong, as there is one example after another of reasoning from a price change:

In a normal recession, the cause eventually self-corrects. Overbuilding leads to a construction slowdown, which leads to lower rates, which leads to new construction. Inventory overshoot leads to destocking, which leads to restocking. The cyclical mechanism contains within it its own seeds of recovery.

No, that’s not how economies adjust to recessions. On average, the sharper the fall in interest rates, the bleaker the outlook for the economy. Yes, falling interest rates occasionally presage a quick recovery, as in 2021, but that’s more the exception than the rule. In fact, economies recover by NGDP rising relative to (sticky) nominal wage rates. Here they forecast the near future:

AI got better and cheaper. Companies laid off workers, then used the savings to buy more AI capability, which let them lay off more workers. Displaced workers spent less. Companies that sell things to consumers sold fewer of them, weakened, and invested more in AI to protect margins. AI got better and cheaper.

A feedback loop with no natural brake.

The intuitive expectation was that falling aggregate demand would slow the AI buildout.

This seems like FDR’s overproduction theory, which confuses a rise in aggregate supply with a fall in aggregate demand. That wasn’t even true under the gold standard, and it is certainly not true in a fiat money world where central banks determine the path of nominal spending.

Here they say something that does relate to aggregate demand:

It should have been clear all along that a single GPU cluster in North Dakota generating the output previously attributed to 10,000 white-collar workers in midtown Manhattan is more economic pandemic than economic panacea. The velocity of money flatlined.

Why does money velocity flatline? Velocity is positively correlated with things like nominal interest rates and nominal GDP growth. If the Fed targets inflation at 2%, then an AI-driven productivity boom will raise nominal GDP growth. Thus, if RGDP growth rises to 5%/year, then NGDP growth would rise to 7%/year. Money velocity would almost certainly accelerate. (Basil Halperin argued that the long-term bond market doesn’t seem to be forecasting that outcome, which suggests that AI may not be as transformative as its proponents assume.)

The bigger problem here is that velocity only matters if the money supply is constrained by something like a commodity price peg. In today’s fiat money economy, a central bank will generally offset any movement in velocity. That adjustment may not occur immediately, and may be imperfect, but Citrini seems to be discussing deep structural forces, not transitory monetary policy mistakes.

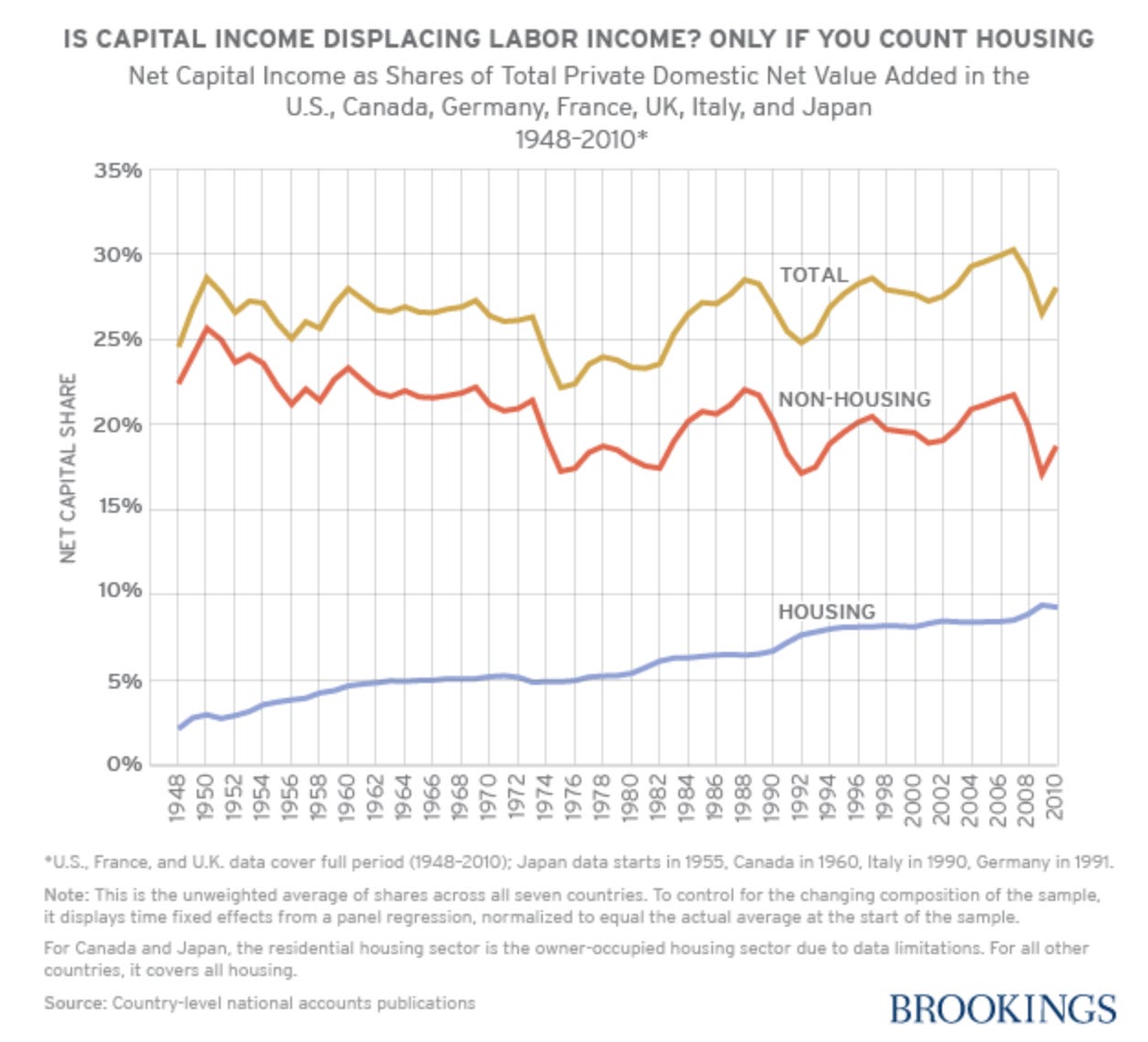

AI does present some issues that are certainly worth thinking about, such as the impact of technology on labor’s share of national income. Here they (misleadingly) suggest that labor’s share has been falling, and is likely to continue falling between 2024-28:

Labor’s share of GDP declined from 64% in 1974 to 56% in 2024, a four-decade grind lower driven by globalization, automation, and the steady erosion of worker bargaining power. In the four years since AI began its exponential improvement, that has dropped to 46%. The sharpest decline on record.

Matthew Rognlie found that the decline is labor’s share is mostly (implicit) housing capital income (from NIMBYism?), and that the share going to non-housing capital is fairly stable:

No, it’s not “globalization, automation, and the steady erosion of worker bargaining power.”

Nonetheless, I could imagine a world where extremely fast AI progress could lower labor’s share, and that this might have important policy implications. But if and when that does occur, it will not be helpful to analyze the situation through the lens of “aggregate demand”.

The output is still there. But it’s no longer routing through households on the way back to firms, which means it’s no longer routing through the IRS either.

Actually, 100% of income is earned by “households”. Companies are owned by households. If you are worried about inequality, then focus on inequality, not aggregate demand.

Don’t take this post as being an exercise in “everything will be fine”. I don’t doubt that AI will create problems, just as other technologies have created problems. I wouldn’t even rule out some sort of AI catastrophe. But overproduction is not the thing we should be worried about. If we ever reach the point where labor is not needed, we’ll all be billionaires—even if it requires a UBI to get there.

Also, my focus has been the macro aspects of the paper. The fact that stock prices moved on the report suggests that they may have some useful insights at the micro level, as some individual firms will be hurt by developments in AI.

PS. I believe Josh Barro came up with the phrase “good things are good”.

PPS. A few weeks ago, I pointed out that tariffs on aluminum were hurting US manufacturing. Just two days later, reports surfaced that the administration might scale back these tariffs. Two days ago, I jokingly suggested that perhaps we should buy Cuba instead of Greenland. Today, I see this Bloomberg headline:

Trump Says He Sees Possible ‘Friendly Takeover of Cuba’

Perhaps Trump reads my blog.

“ The fact that stock prices moved on the report suggests that they may have some useful insights at the micro level, as some individual firms will be hurt by developments in AI.”

The fact that stocks moved down at the macro level suggests that there are not enough thoughtful posts about macro implications of AI like this one.

Good point on the need to focus on inequality arising from the (AI-induced) rise in stock prices. Capital gains, and associated income, do not seem to be well captured by traditional national income accounting as far as I can see.

https://users.nber.org/~robbinsj/jr_inequ_jmp.pdf